-

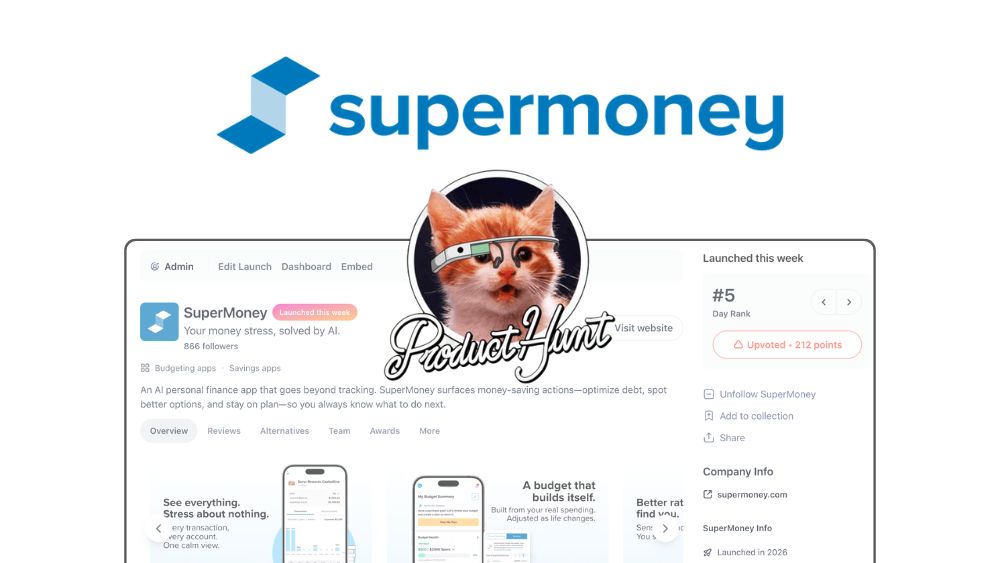

SuperMoney Launches AI Financial Assistant

SuperMoney launched it’s AI personal finance assistant on Product Hunt this week and made it to the top 5 of the day!

We started SuperMoney in 2013 as a financial product reviews marketplace. I thought it was wild that there was no real transparency about financial products. Fortune 500 companies apparently agreed, sending us cease and desist letters in the early days. We kept going anyway and over 2M people became members.

The problem we kept coming back to: traditional financial advisors operate on an assets under management model, so they’re built for the top 1%. Everyone else is dealing with real financial stress and getting no guidance at all. Nearly 9 in 10 Americans started 2026 feeling financially stressed, according to the National Endowment for Financial Education. We’ve spent years building toward what we always believed AI could make possible.

The SuperMoney app connects your accounts and actually does something with the data. Not just pretty charts. It:

- Builds your budget, tracks your spending, sets goals, and suggests what to do next to achieve them.

- Serves you a live feed of insights based on what’s actually happening in your finances.

- Surfaces lower rates on your existing loans and smarter debt paydown paths. Real savings, not just insights.

- Lets you ask questions directly. The AI knows your accounts, your credit, your loans, and your goals, so the answers are actually relevant to you, not generic advice you could Google.

Try it out at SuperMoney.com!

-

SuperMoney Unveils Loan Offer Engine at Finovate Spring 2017

We were super excited to demo our brand new loan offer engine at the prestigious Finvoate fintech showcase conference in San Jose.

Within the personal loan industry alone, there are literally hundreds of lenders to choose from and all of them are different. You can go from lender, to lender, to lender, filling out applications to try and find your best option but that’s a ton of effort. Lending aggregators popped up to solve this problem by ‘matching’ borrowers with lenders.

But the dirty little secret behind most loan aggregation websites is that they run on a ping tree model. Ping trees chuck borrowers down a lead delivery waterfall attempting to sell the lead to the highest bidder. If the highest bidding buyer rejects the lead, the system attempts to sell to the next buyer with the borrower ultimately being sold to whoever will pay the most for that lead. This ping tree model works quite well for the aggregating site, as it’s rigged to produce the highest payouts. But as you could probably surmise, the “matches” produced by Ping Trees seldom connect consumers with the loans that are most financially beneficial to the borrowers themselves.

When consumers shop for an airline ticket they expect real offers in real-time. Well, we’ve brought that great Kayak-like comparison shopping experience to financial services. Our Loan Offer Engine transparently allows consumers to submit a single soft-pull loan application to all the leading online lenders and returns real loan offers back. SuperMoney users can transparently discover the best option based on their needs and that serve their best interest.

SuperMoney is a two-sided marketplace platform with consumers looking for financial services on one end and financial service providers on the other. On the financial services side, we have a wide array of financial verticals represented in our publicly accessible reviews website. Within the personal loan offer engine, we are currently partnered with leading marketplace lenders, direct lenders, and banks. We aim to extend the platform to integrate credit unions and other players in the ecosystem not currently represented.

We are soon launching the same great loan offer engine experience in the auto lending vertical and aiming to follow that up soon after with a mortgage version. Our goal is to extend the framework we developed into all lending related verticals initially, and then to other financial services where consumers can benefit from apples to apples comparisons and transparency.

Our goal is simple. To build the brand consumers think of first whenever they need a financial service. We aim to get there within two years.

-

Expert Interview with Miron Lulic on Personal Finance Advice for Mint

This interview was originally published by Mint.com.

SuperMoney isn’t your typical personal finance site: With a theme of superheroes and villains, it teaches personal finance in a fun, dynamic way. We spoke with founder Miron Lulic about SuperMoney and personal finance.

What brought you to writing about finance?

I read some startling facts about how big of an issue basic financial literacy was in America. A 2012 studyfound that two in five adults give themselves a C, D or F on their personal finance knowledge. I wanted to build something to help solve this problem. So I built SuperMoney – a platform for people to share all the world’s personal finance knowledge. Our mission is to organize all this knowledge into the most transparent and honest source of good financial advice.

SuperMoney has a playful theme of superheroes and villains. Why’d you choose that as your approach?

When you think about consumer finance, you probably think boring and colorless. If we’re going to get people excited about the topic, I felt we needed to make our brand as consumer-friendly as possible. After all, the worst thing we could do is to make personal finance intimidating. So we went with a playful superhero theme to make things a little more accessible. Our brand mascot is Captain Money, and he’s in a battle against the Evil Debt Blob to “Super Power Your Finances.” Captain Money is an advocate to the consumer, helping to guide their decisions through content, reviews and Q&As.

What are some common misconceptions about personal finance you often run into?

People are far too willing to adopt constraints. They say to themselves, “I just don’t have any money to invest at this time.” As a result, they fail to ever get the wealth-building process started. The truth is, you don’t need a lot of money to get started building wealth. I recently wrote an article about breaking free from these self-imposed constraints in “How To Turn $5 Into Your Dream Company.”

Another common misconception is the belief in quick fixes. Rather than build a solid foundation, many neglect to put any plan in place and seek out instant solutions to their problems when they arise. For example, rather than have an emergency savings fund, they take out loans to deal with unexpected financial needs. Often the debt gets out of hand and they end up settling their debts or look to other quick solutions. Similarly, they seek get-rich-quick schemes to build wealth rather than adopting long-term strategies. The right approach is quite the opposite. I recently wrote about it in “The Secret to Why Most Endurance Athletes Are Wealthy & Successful.”

Personal finance is all about setting goals and working hard to achieve them. It’s a long-term process that requires a combination of strategies. Most people either don’t get that or choose to ignore it. We try to educate them with simple strategies they can adopt without much friction.

Is there a common financial mistake you see a lot among people, and how can it be avoided?

People like to tell themselves that they will save more later in life, when they have more income. But even if they get a raise, they tend to just increase lifestyle expenses rather than allocate it to a retirement plan, for example.

If this is you, the solution is to first be honest with yourself. Every year you put off investing makes your ultimate retirement goals more difficult to achieve. In fact, the amount of capital you start with is not nearly as important as getting started early. This is due to the power of compound interest. Time is the primary ingredient to the magic of compounding. The sooner and more aggressive you start, the more powerful the result.

Secondly, you should adopt a strategy that will automatically nudge you into the right direction. For example, many companies have adopted “save more tomorrow” retirement savings options into their 401(k) programs. This allows employees to make a commitment today to allocate a portion of future salary increases toward retirement savings. There are many “personal finance hacks” like this that can have a major impact.

What’s the single best piece of financial advice somebody’s ever given you?

Pay yourself first. Too many people treat savings and wealth building as the bonus money that comes after you’ve paid your expenses. They should instead take some time to find out their long-term retirement goals. When they determine how much they should be saving, they should then make sure they are automatically deducting this amount to fund a 401(k) or other savings vehicle. Find ways to reduce your expenses so they can work around your savings, and make sure you pay yourself first!

Where do you see personal finance headed in the next few years?

There have been many amazing personal financial management products to emerge in the last 10 years. The sad truth is that only a small fraction of the population leverages them. I think we’ll see these tools get smarter and easier to use with much more widespread adoption. Additionally, I think we’ll see them embedded into many of the financial firms themselves. This is the path LoanNow is taking by turning loan repayment into a rewarding game-like process. Borrowers unlock achievements to help raise their credit score or even reduce their interest rates. Their end goal is to incentivize loan repayment through personal finance education.

Keep up with the latest from SuperMoney on LinkedIn and Twitter.

-

A Growth Mindset Team: The Secret Formula

Looking back at my childhood I was often resentful of my mother’s form of praise. I would bring her my graded tests and if I handed her something with a 95% score, she would give me a kiss and say ‘That’s my boy, next time try harder and you’ll get 100%!’.

I often thought to myself ‘you’re not satisfied?’. Little did I know I was developing an attitude about the world known as “growth mindset”.

This is a term coined by Stanford professor Carol Dweck. Carol discovered that how we praise our children is just as important as how often. The right sort of praise can help your child foster a growth mindset and boost his or her motivation, resilience and learning. The wrong kind can create self-defeating behavior.

The Fixed Mindset

When you praise intelligence you appeal to a fixed mindset – the belief that intellectual ability is innate. Those with a fixed mindset tend to agree with statements such as “You have a certain amount of intelligence and cannot do much to change it.” They see mistakes as failure and as signs that they aren’t talented enough for the task. More concerning, they tend to avoid challenging tasks. The desire to learn becomes secondary.

The Growth Mindset

When you praise for effort, you appeal to a growth mindset – the belief that you can develop ability through controllable effort. Those with a growth mindset believe that they can get better at almost anything, as long as they spend the necessary time and energy. Instead of seeking to avoid mistakes, they see mistakes as an essential precursor of knowledge.

Growth Mindset Praise In Work Culture

Startup organizations tend to attract growth mindset individuals who are risk averse, willing to wear many hats and put in the effort to win. In my startup teams I’ve seen this dynamic emerge serendipitously – sort of a mutual understanding between like minded individuals.

The opposite seems to be true of larger organizations that seem to breed complacency. The largest organization I’ve worked in was around 1000 people. The company had a top-down management approach that did little to foster a growth mindset culture. It’s not a place I was able to stay at for long.

Why Is Growth Mindset So Important?

First, if fixed mindset dominates your work culture, your employees will believe company success is due to factors outside of their control. Similarly, they will think of failure in the same way. They will perceive mistakes as failures rather than learning experiences. This will affect their willingness to take on challenges that may otherwise move the organization forward.

Second, perhaps as a reaction to the first, they will become more concerned with looking smart than with value creation.

Third, they will be less willing to confront the reasons behind any deficiencies, and less willing to make an effort. Such team members will have a difficult time admitting errors. There is too much at stake for failure.

How To Develop Growth Mindset In Your Team

1. Praise Effort

Cite specific behaviors such as the amount of time spent or the approach your team member is taking to tackle a problem. This will enable them to connect their actions with results.2. Praise Failure

If your team member works hard on a challenging project that ultimately doesn’t do well, treat it as a learning experience. Thank them for being so dedicated and let them know it’s ok to fail. If the project still has hope, offer to work together to figure out how to make it work.3. Reinforce New Experiences

If your team member is attempting a new challenge reinforce the positives of new learning experiences. For example, “It’s impressive you are taking the time to learn this new programming language – I know you haven’t done this before.”4. Encourage Curiosity

Embrace the adage “There is no such thing as a stupid question”. Let your team members know you value their quest for knowledge and exploration of new ideas.Conclusion

Whether you’re 10 years old or 50, positive reinforcement has a major impact on your mental health. As adults we spend most of our waking life at work. As such, it’s important that we all receive praise from our leaders and colleagues. It’s equally important that we foster work culture that embraces growth mindset praise. We should position reinforcement in a way that empowers our team members to grow.

-

The Secret To Why Most Endurance Athletes Are Wealthy & Successful

Endurance athletes earn almost three times as much as the general population. Not 50% more. Not 100% more. Almost 300% more money on average!

According to the New York Timesthe average ING New York City Marathon runner’s household income was $130,000. USA Triathlon reports the average triathlete’s household income is $126,000. A 2006 Runner’s World subscriber study indicated their average subscriber had a household income of $139,000 and average household net worth of $943,000.

In comparison, the average 2012 US median household income was just $51,017.

There is an obvious correlation between endurance sports and wealth building habits. Endurance sports and wealth building are both character driven activities that require goal setting, focus, commitment, perseverance, and good old fashioned hard work. It takes a lot of commitment to reach your potential in both endurance sports and in wealth building.

What makes these “wealthletes” different?

Trait # 1: Set Big Goals

Some of us have far off dreams – wealthletes set goals.

They don’t just talk about their goals. They set specific but challenging goals, assess their goals, and go after them with courage and determination.

Wealthletes overcome procrastination by setting meaningful and challenging goals. This sort of goal setting happens both long term and short term. A full 26.2-mile marathon is a long way to run, but it’s the 500-miles of training over five months where the work is done. A typical training schedule consists of many smaller milestones that progress in difficulty over the training period. Furthermore, a marathoner will also typically break up his race day run into a set of segments or mini-goals to mentally achieve their ultimate race day goal. Setting big goals and being able to break them down into manageable goals is the essential first step.

Wealthletes also take time to assess their goals by asking questions like, “Do I really want this goal?” If the answer is yes, they close off all distractions and find a way to win. They keep running the race until they cross the finish line.

It’s great to have goals but it’s also essential to give them your all. The best don’t give 50% to their goals. They don’t give 75%. They give 100%. Self-sacrifice and self-discipline are more than words to the champion. They are a way of life.

Trait #2: Don’t Think Short Term

Wealthletes don’t think short term. They understand that the odds of winning the Powerball lottery is about 1 in 200 million and get rich quick schemes generally have similar odds. They don’t waste time looking for instant success strategies like the masses. Instead, they do the daily work required to reach the finish line.

Wealthletes also accept that reaching a goal is 20% perspiration and 80% determination. They lace up their shoes each day and get out that door whether they feel like it or not. Wealthletes are generally people who work harder, try harder, and refuse to quit.

Trait #3: Build A Support Group

The most effective road to success is to surround yourself with people who have already mastered what you want to accomplish – and then learn from them.

In endurance sports this sometimes means joining running clubs or maybe finding other road bike riders to push you forward on those 50-mile weekend rides.

Having a team behind you to help guide you and motivate you is very valuable both in endurance sports and wealth building.

Whether it’s discussing financial strategies with friends, working with a financial advisor to stay on track, or staying active in communities like SuperMoney, the Wealthletes among us build a team to support them.

Trait #4: Benchmark and Monitor Their Success

The image of a runner checking their mile per minute pace on a digital watch is almost cliché. Monitoring performance is something all serious athletes do. These days we have amazing benchmarking tools like Strava – a smart phone app that tracks your running, biking, or even swimming metrics and shows you how you stack up against everyone else who has ran that same segment.

This sort of personal benchmarking is key to the wealth building process. Those who know how to grow wealth know how to analyze their efforts to do so. It used to be a lot more complicated and tedious to do so, but these days we have so many tools at our disposal to automate the process. Tools like Check, SigFig, WealthFront, and other money management tools.

Trait #5: Pace Themselves to Victory

Many people give up on their dreams a few steps from the finish line. Wealthletes don’t. They pace themselves to win the race.

Wealthletes use their energy wisely. Their smart “even” pacing brings them to the finish line in record time ahead of the pack. Wealthletes pass other people near the finish line because they run hard and smart.

The old adage ‘slow and steady wins the race’ holds true to wealth building.

Trait #6: Pick Themselves Up When They Fall

Running injuries and the like are common among endurance athletes.

Wealthletes don’t give up when things don’t go their way. They treat failures as learning experiences and to get back into the race as soon as possible. They do so with courage and with conviction.

Trait #7: Leverage Worry and Fear

Worry is interest paid on trouble before it is due.

Wealthletes learn to harness fear by developing a strong backbone – not a wishbone. They don’t “wish” for success, they work at success in spite of their fears.

Wealthletes stay mentally and spiritually strong in the face of adversity in difficult and painful circumstances. They replace worry and fear with determination. Wealthletes run their race to win regardless of the obstacles that stand in their way.

Trait #8: Go The Extra Mile

Wealthletes consistently run the extra mile. Those few extra steps each day separate Wealthletes from the rest of the pack.

Wealthletes are willing to do the little things that the masses are unwilling to do. They complete their daily workouts in all kinds of weather conditions. They run when they don’t “feel” like running. Wealthletes understand that short-term pain produces long-term gain.

Wealthletes forgo a few pleasures today for greater rewards tomorrow. They train consistently to win the race regardless of the circumstances. Going the extra mile each day keeps wealthletes out of the maze of mediocrity.

8 Questions To Ask Yourself

- How much time and effort are you giving to your most important wealth building goals?

- Are you taking the path of least resistance to reach your wealth building goals?

- Are you surrounding yourself with people who are helping you reach your wealth building goals or people who are steering you in the wrong direction?

- What are you doing to monitor your wealth building success?

- Are you pacing yourself effectively in the wealth-building race?

- Is it time for you to get back into the wealth-building race?

- Are you pushing through your fears in the pursuit of your wealth building goals?

- What extra steps do you need to take today to improve your chances in the wealth-building race?

The Finish Line

In summary, the traits of endurance training and wealth building are remarkably similar.

Both require smart goal setting, long-term thinking, a support team, constant benchmarking, self-pacing, picking yourself up when you fall, conquering worry, and going the extra mile.

The lesson is clear – expediency is not the solution. Get-rich-quick thinking and instant gratification are not the way to build wealth. Instead, by practicing basic principles of goal setting, hard work, and self-discipline, you will build wealth throughout your life.

It is no coincidence that endurance athletes are more financially successful than the general population. They understand the basic principles required to reach your goals.

There are no short cuts to success.

This article was originally published on SuperMoney by Miron Lulic.

-

Home Ownership: Is It Really Worth It?

Recent Gallup polls show that Americans still believe the best “long-term investment” is real estate. Most Americans rank real estate investment ahead of mutual funds, stocks, bonds and other options. This news is somewhat surprising considering the fact that so many Americans lost everything they had in the wake of the recent housing collapse. Could everyone be wrong?

Real Estate Isn’t Always a Good Investment

Never mind the recent real estate bubble. Over an even longer horizon, the numbers don’t look so good either. In the past century, housing prices have grown at a compound annual rate of just 0.3 percent once one adjusts for inflation. Over the same period, the Standard & Poor’s 500-stock index has had comparable annual returns of about 6.5 percent.

So why does there continue to be all this romanticizing over home ownership? Some believe that people feel more secure investing into something that is tangible. A home is a large investment, but it is one that can actually be seen and measured by how much material and time went in to building it. Other investments are usually only seen as words on a piece of paper. For example, when you invest in the stock market and purchase 100 shares of McDonalds, it is not as if Ronald himself shows up at your door to deliver you an equivalent amount of cheeseburgers or Happy Meals.

Foolish Faith or Worth It?

Due to the hype that surrounds home ownership, many people end up foolishly buying more house than they need. This can start a snowball effect by tie-ing up all their cash flow, keeping them from diversifying into other investments, and also resulting in higher than necessary maintenance costs and general up-keep.

Many people are beginning to shift their opinions on real estate investments and lose a bit of the allegiance toward this great American dream of home ownership. According to surveys done in 1996, nearly 90% of Americans believed it was better to purchase a home rather than rent one. When asked that same question 5 years later, the number fell sharply to only 63%, and many people began to refer to it as the great American nightmare rather than dream.

Proponents of real estate investment will argue that real estate return on investment is misrepresented due to other factors such as tax credits. The United States tax code pushes people towards home ownership by offering tax incentives for first time home buyers, and other tax credits for those who own a home. After all, we all have to live somewhere, right?

The Rent vs. Mortgage Argument

But despite the recent trend away from investing in home ownership, there are still many people who defend it as the best option for putting your money to work for you. People might argue that while purchasing a home is a considerable investment, the money used to pay off the mortgage each month is comparable to what they would have otherwise paid towards rent if the person did not own their home. The main difference in putting that money towards owning a home rather than renting one is that in 30 years when the mortgage is paid off you actually own the property, as opposed to a rental where the equivalent amount of money paid each month would result in an investment gain of zero after 30 years.

Another valid claim in favor for home ownership is the fact that while the housing collapse hit the entire nation with financial and economic strife, there are still many places in the US that are showing great economic success. Investing in real estate in an area that is continuing to grow and show signs of economic success can result in a very high return on your investment over time. In these regions, there are many people who purchased their home 30-40 years ago for somewhere around $35,000, who now sit on that same investment valued today at over $1 million dollars.

Many people who support property investment over other traditional investments also point out that while the real estate market did suffer its’ recent crash, the stock market also faces the same, if not higher, risk of crashing. People lose millions of dollars invested into the markets on a regular basis, just based on poor choices alone. But even if the real estate market suffers a great down turn, you never end up losing everything– you still own your house. Many would argue that over time the best investment for Americans continues to be owning a little piece of that dream.

By The Numbers

Let’s look at a typical example and run the numbers to get an idea about return on investment. According to census.gov, the March 2014 median average sales price of new homes in United States is $290,000. From deptofnumbers.com, the US median residential rent was $884 in 2012.

Let’s take these numbers and compare the relative outcome of investing in a home through a standard 30-year fixed mortgage at a current 5% interest rate versus taking the down payment and investing in the stock market.

Here’s a full list of assumptions:

- Purchase Price $290,000 (US median new home price 2014)

- Down Payment $58,000 (20% down payment)

- 30 year fixed mortgage ($232k at 5%)

- Total estimated closing costs $5,440

- 6% commission paid to brokers

- 3% real estate appreciation per year (10x the last century’s average)

- Income tax rate 25%

- Current monthly rent $884 (US median 2012)

- Expected rate of inflation 3% (for future rent and property taxes)

- Rate of return on investments 6.5%

We calculated the break-even point by examining how long it would take to create enough equity in this home to exceed the value of investing our initial down payment. We also accounted for differences in monthly rent and house payments–if our rent payment is less than our net house payment, we add that monthly savings to our investment. If our house payment is less than our rent payment we subtract that amount from our investment.

Year House Payment (PITI) Payment After Tax Savings Rent Payment Value of Investment Home Equity 1 $1,807.93 $1,509.11 $884.00 $75,265 $52,201 2 $1,824.81 $1,527.90 $910.52 $87,763 $64,222 3 $1,842.19 $1,547.34 $937.84 $100,974 $76,680 4 $1,860.09 $1,567.45 $965.97 $114,944 $89,592 5 $1,878.53 $1,588.24 $994.95 $129,719 $102,976 6 $1,897.52 $1,609.75 $1,024.80 $145,351 $116,849 7 $1,917.08 $1,632.00 $1,055.54 $161,892 $131,232 8 $1,937.23 $1,655.02 $1,087.21 $179,401 $146,143 9 $1,957.99 $1,678.84 $1,119.82 $197,937 $161,605 10 $1,979.36 $1,703.48 $1,153.42 $217,566 $177,639 11 $2,001.38 $1,728.98 $1,188.02 $238,357 $194,267 12 $2,024.06 $1,755.37 $1,223.66 $260,383 $211,513 13 $2,047.42 $1,782.69 $1,260.37 $283,723 $229,402 14 $2,071.48 $1,810.95 $1,298.18 $308,460 $247,959 15 $2,096.26 $1,840.21 $1,337.13 $334,683 $267,212 16 $2,121.79 $1,870.50 $1,377.24 $362,488 $287,188 17 $2,148.08 $1,901.86 $1,418.56 $391,974 $307,917 18 $2,175.16 $1,934.32 $1,461.12 $423,250 $329,428 19 $2,203.05 $1,967.93 $1,504.95 $456,431 $351,754 20 $2,231.78 $2,002.74 $1,550.10 $491,638 $374,927 21 $2,261.37 $2,038.78 $1,596.60 $529,001 $398,983 22 $2,291.85 $2,076.11 $1,644.50 $568,659 $423,956 23 $2,323.24 $2,114.78 $1,693.84 $610,761 $449,886 24 $2,355.57 $2,154.82 $1,744.65 $655,463 $476,810 25 $2,388.88 $2,196.31 $1,796.99 $702,933 $504,770 26 $2,423.18 $2,239.29 $1,850.90 $753,350 $533,809 27 $2,458.51 $2,283.82 $1,906.43 $806,905 $563,972 28 $2,494.91 $2,329.96 $1,963.62 $863,800 $595,304 29 $2,532.39 $2,377.78 $2,022.53 $924,253 $627,855 30 $2,571.00 $2,427.33 $2,083.20 $988,493 $661,672 In 30 years the value of our investments made while renting has grown to $988,493 while our home equity has grown to only $661,672.

A difference of $326,821!

As you can see, it is quite possible to earn a better return on your initial down payment investment even when accounting for rent payments and those highly sought after home ownership tax credits.

But Wait There’s More! Insurance, Association Fees, Maintenance and Repair Costs

There are many other costs associated with home ownership beyond the mortgage. Insurance is an essential, unavoidable and costly part of having a home, and HOA fees add up to a lot of money very quickly. Even if you’re lucky enough to not have association fees, you’ll still end up spending a loads on general maintenance. Then come the inevitable repairs – the broken hot water tank, the leak in the roof, mold damage. These can be a substantial burden when they creep up for the property owner, but are things renters don’t have to worry about.

Opportunity Costs of Home Ownership

Holding a mortgage is a large liability that limits your freedom in many ways. We are living in a time where we need entrepreneurs more than ever but fewer than ever are willing to take the risk.

Job security to satisfy mortgage payments is the reason most are unwilling to take on the risk of starting a new business – one of the quickest ways to acquire wealth. By taking on a massive liability like a mortgage you end up having to mitigate risk from other places in your life. The fear or failing in a new venture and subsequently threatening the good standing of their mortgage is enough to scare most people away from ever even trying.

The Intangible Cost of Decreased Mobility

Many people discount the value of mobility that renting affords. If you want to live an adventurous lifestyle and move somewhere else in the country, or perhaps another country, mortgages add an additional layer of complexity that is enough to keep people from pursuing their dreams abroad.

So What’s The Right Answer?

So, what is the answer to this growing debate over whether you should invest your hard-earned money into real estate or not?

There are 2 main financial advantages of home ownership:

- Tax advantages from the mortgage interest write off (this is a big bonus of home ownership if you have a high tax rate)

- Home Appreciation: This is completely a function of timing your purchase. You can lose or win based on the price you pay for the home. If home prices are high, renting is probably the best bet. If home prices are low, you could have strong ROI on your investment. That being said, some argue that with an aging Baby Boomer demographic and Millennial / Gen-Y demographic disenfranchised with home ownership, we are more likely to see a real estate market that goes sideways in the coming decades similar to what occured in Japan after their 80s real estate crash.

A home purchase is likely the biggest single purchase someone makes in their life, so they should really take time to understand the local and broader markets before making such a huge decision. There are many mistakes that people could make that would cause their real estate investment to be a less than favorable one. Rushing into home ownership, buying in a region that is failing economically, getting sucked into a loan that is less than optimal, or even being uneducated or less informed about your options could result in a negative outcome.

The advantages of home ownership can be easily outweighed by the additional costs of maintaining a home, taxes, utilities, improvements, etc. From that perspective a home can be a big money pit.

Furthermore, if one is disciplined enough to take that net cash flow they would be putting towards a mortgage and instead invest it in a higher ROI investment, they can definitely do better with their money regardless of tax incentives, rental costs and the other factors we have discussed.

There are of course the intangible advantages of comfort, security, stability, privacy achieved by owning a home. Those are hard to put a value on and, and arguably they can be mitigated with a good lease agreement.

While there is still no guarantee that your money will be safe anywhere you put it, investing into home ownership continues to be a relatively safe option. The important factor in the success of this investment comes down to the owner himself. If someone is well-informed, patient and wise in making their decision to buy a home, they will find a much higher return on their investment over time.

The best advice is always to research your options before jumping into anything. Know all the options available to you before choosing to buy a home. Once you are ready, make sure you do not bite off more than you can chew, and instead focus on purchasing a home that is appropriate to your needs. Remember, the bigger the house, the more problems and subsequent costs you may run into. After all, a well informed investor is often a happy investor, (and sometimes home owner, too!).

Home Ownership: Is It Really Worth It? was original published on SuperMoney by Miron Lulic.

-

How I Raised My First $100K

I think a lot of would be entrepreneurs have a glorified view of venture capital fundraising. That you come up with a great idea and somehow go into a meeting, pitch, and get a check. It may have very well happened like that at the peak of the dot com boom, but based on our experience, probably very seldom happens like that now.

Fundraising is a pain in the ass for entrepreneurs. It takes a tonne of time and is a huge distraction.

This is the story of my first real venture capital fund raising experience.

The startup was Swagsy and we were building a celebrity curated shopping experience where tastemakers brought their fans and followers sweet deals on their favorite products and services.

We had been working on Swagsy for over a year but got serious at the tail end of 2011. I had built an early prototype that, in hindsight, we should have went to market with in order to stay lean and test our hypothesis on the cheap. But I suffer from the same sense of idealism that a lot of product guys do – I wanted Swagsy to be awesome. So my co-founders and I decided to invest our own money into Swagsy and bring on some additional development help.

By March we were armed with a very slick alpha product. Our business dev efforts had delivered some early commitments from celebrities and brands. I had also managed to build out the team with some very talented people who joined us on either an equity or commission only basis. We had also put together an impressive set of advisors who could help us along our journey.

We decided it was time to raise money.

In late March 2012, I scheduled a lunch with our advisor Jody Sherman to discuss our fundraising plans. Jody was very clear about his opinion, “Forget about fundraising for now – just launch!”

My opinion was that we had taken Swagsy far bootstrapping and while we hadn’t ‘launched’ we had traction in other forms as well as budding investor interest. I didn’t need to prove end user traction, right?

Knowing that we had some loose ends to tie up on the product side and had more business development work to do, we moved forward with our fund raising efforts.

I feverishly worked on a slick deck that was inspired by the open sourced by DressRush deck. Of course I also spent a lot of time creating detailed financial models that outline how much capital we would require, our use of funds, and all sorts of assumptions.

We were armed.

We set up meetings with a smorgasbord of angel investors in both the technology and entertainment communities. We pitched at angel group events. We met with accelerators. We even took meetings with a few early stage VCs. Our efforts spanned both northern and southern California.

It was a huge undertaking to go on all these first and second dates and we spent over three months doing it. They all seemed to have gone extremely well. Everyone was saying the same thing. They thought we had a good idea, they were impressed by our alpha product, and thought we had a strong team with complimentary skills. We were feeling like real players.

But then came the eventual ‘We are interested in investing but want to see what happens at launch’. We came to realize that there was a common concern about whether we could actually execute on this grand plan. I guess that I can see why people might think we’re a little audacious – or crazy – to suggest we’ll get a bunch of celebrities to cooperate. And to be frank, it was. Getting a group of celebs to cooperate on a project is like herding a group of wild cats.

In late May / early June of that year we realized that all of our attention was going into fund raising and the rest of the business was suffering. It was time to scale back our efforts.

One of our close angel investor contacts had already made a commitment for $100k very early in our process but our goal was to raise $1 million to get the company off the ground. We reluctantly realized we should have taken that $100k and focused on getting our minimum viable product to market rather than chasing investors for 3 months.

So we decided to sign a convertible note for $100k, walk away from fundraising and go back to building the business.

While I think that our timing was off, I don’t feel that our time was wasted. We learned our lessons.

Lesson #1 – Never meet with VC’s unless you are 100% ready to fundraise. We were almost there but weren’t quite there. Our efforts would have been better focused on building the business and getting to launch.

Lesson #2 – Focus on the right investors. Being fairly new to the fundraising process, we spent a lot of time meeting with people that were not a good fit. The stage of our business was far beyond the value add an accelerator could provide and the terms at which they invest wouldn’t make any sense. This was hit home by Howard Marks, Co-chair of the LA based accelerator Start Engine, who simply responded to our pitch with a “Why are you here? You don’t need an accelerator”.

Lesson # 3 – It’s not just the stock market that is focused on short-term results. We hear all the time about how Wall Street is too focused on today’s earnings rather than investing in tomorrow’s opportunities for growth. Well this is becoming the norm for early stage venture capital as well. These days traction outweighs ideas, team, or product. Investor interest will absolutely be affected by how your business performs during the months they are considering investing in you.

Ultimately we did go to market with a beta Swagsy product. We built a great beta site and a ran small pipeline of ‘flash sale endorsements’ using celebrity curators.

However, in the end our hypothesis was wrong. The economics of the performance-based endorsements business model just didn’t equate to a scalable business. Celebrities had unrealistic expectations for upfront and post sale payouts when, in reality, a celebrity micro-endorsement via social media does very, very, little to push product.

We could have tested our hypothesis for a lot less money by following lean startup methodology. But we were blindly chasing the startup dream.

I’ve had lots of time to reflect about the experience and I have no regrets. I also don’t look at it as a failure because, as torturing as it was, the experience was priceless and I learned more about startup life, the inner workings of Hollywood, and the venture capital economy than most will ever have an opportunity to.

Success is nurtured by failure.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.

You must be logged in to post a comment.